2025 brought welcome relief for Kiwi borrowers, with rates softening and stability returning. But in 2026, the mood is shifting.

The Official Cash Rate (OCR) is currently sitting at 2.25%. Most economists expect it to stay there for the majority of the year. However, with inflation running hotter than forecast (CPI, 23 Jan 2026), many are now predicting rate hikes to arrive sooner than originally expected – possibly by early 2027, if not before.

This year will be all about watching for signs that the Reserve Bank is ready to move.

Note: Bank OCR forecasts are highly responsive to shifts in inflation data and can change quickly as new economic information emerges.

2026 offers an opportunity to be proactive with your mortgage strategy. With rates holding for now, smart structuring can help you stay ahead if the tide turns.

Take a strategic approach to refixing

Longer-term rates may offer greater certainty if increases are ahead

If your repayments drop, keep them the same

This helps reduce the life of your loan and the interest paid

Consider splitting your loan

A mix of fixed terms can help manage interest-rate risk while giving you more flexibility as the market shifts. It’s a smart way to balance certainty now with options later.

Explore cashback and refinancing incentives

Many lenders are still offering cash back incentives of up to 1% for new loans and refinances, subject to meeting minimum lending criteria.

For example:

A $500,000 loan could mean up to $5,000 cash back when refinancing.

We’re seeing clients use these cash backs to offset break fees, making it easier to switch to more competitive rates or lock in longer fixed terms while conditions are still changing.

The housing market is expected to perform well in the first half of 2026, fuelled by economic growth and stronger lending activity. But the second half may slow, as election uncertainty and potential rate rises start to affect buyer confidence.

Why the market could cool:

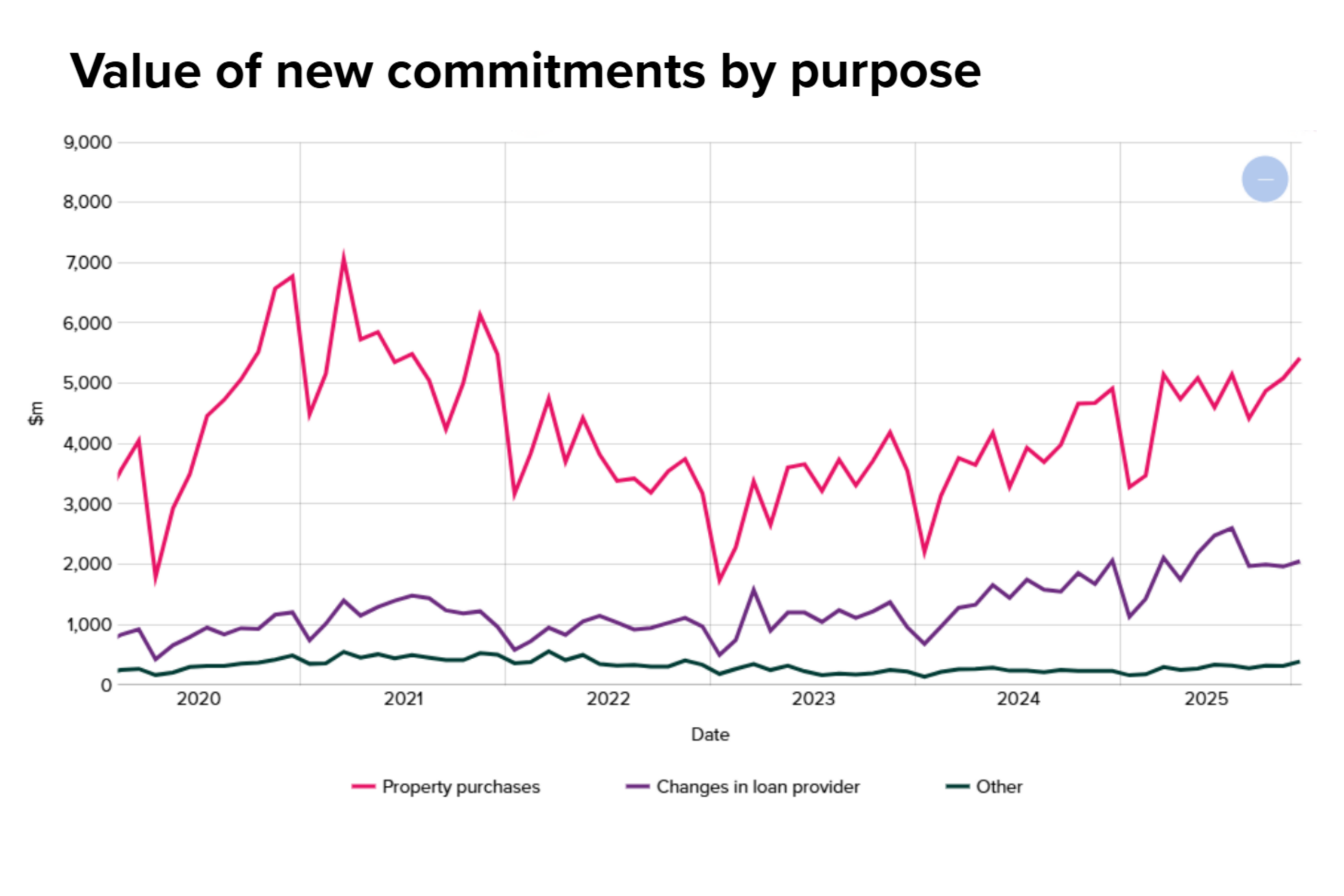

Source: https://www.rbnz.govt.nz/statistics/series/lending-and-monetary/new-residential-mortgage-lending-by-purpose

Source: https://www.rbnz.govt.nz/statistics/series/lending-and-monetary/new-residential-mortgage-lending-by-purpose

Uncertain about fixing, floating or refinancing? Let’s talk it through – our mortgage advisers are here to help!

Chat with an Enva adviser today! Email us at mortgages@enva.co.nz or give us a call on 0508 287 672

Disclaimer: This blog is for general information only and does not constitute personal financial advice. Always speak to a qualified financial adviser before making decisions related to your mortgage.

Share this article

Share this article

Fill out your details below and we’ll be in touch soon.

"*" indicates required fields